By Isa Jane D. Acabal

YIELDS on Philippine government securities fell last week due to strong demand and as investors expect the central bank to cut interest rates sooner following a sharp slowdown in economic growth.

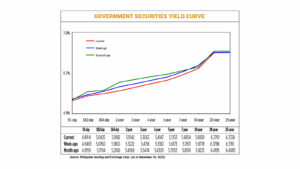

Benchmark yields fell by an average of 7.3 basis points (bps) week on week, according to PHP Bloomberg Valuation Service reference rates as of Nov. 14. The drop was broad-based, covering short-, medium- and long-term tenors, although late profit-taking trimmed some gains.

At the short end, yields on the 91-, 182- and 364-day Treasury bills slipped 4.89, 3.35, and 7.18 bps, respectively, to 4.8914%, 5.0425%, and 5.1082%. Yields on medium-term bonds — those maturing in two to seven years — also dropped, with the biggest declines seen in the two- to five-year securities. The seven-year bond followed with a slightly smaller decrease.

At the long end of the curve, yields on 10- to 25-year bonds also slipped, though by smaller amounts. Trading activity fell sharply from the previous week, showing investors turned cautious after the mid-week rally.

“The weaker-than-expected GDP (gross domestic product) print contributed to a strong bid in the first half of the week, driving yields lower particularly at the front end, as markets priced in a softer growth outlook and the possibility of earlier policy easing,” Lodevico M. Ulpo Jr., vice-president and head of fixed-income strategies at ATRAM Trust Corp., said in a Viber message.

The economy expanded 4% in the third quarter, the slowest in more than four years. The disappointing result shifted expectations toward earlier rate cuts by the Bangko Sentral ng Pilipinas, with some traders speculating that the Monetary Board might not wait until its scheduled meetings.

The tone was reinforced on Tuesday when the Bureau of the Treasury fully awarded P22 billion in Treasury bills as bids swelled to P98.31 billion, more than four times the offer. The strong demand pulled short-dated yields lower and encouraged fund managers to lock in remaining carry, analysts said.

“Market participants likely tried to lock in yields, with the dismal third-quarter GDP growth reading spurring further rate cut expectations,” Marco Antonio C. Agonia, an economist from the University of Asia and the Pacific, said in an e-mailed reply to questions.

A bond trader noted that early-week optimism extended across maturities. “Initially, yields dropped on bets the BSP will cut rates, and some quarters even looked at the possibility of an off-cycle adjustment given the drop in equities,” the trader said.

However, part of the week’s rally faded on Friday after profit taking, especially in the four- to 10-year tenors, which nudged yields slightly higher from the previous day. “Political risks from the flood control scandal resurfaced,” Mr. Agonia said, adding that this triggered caution on the middle and longer sections of the curve.

Mr. Ulpo said the market’s tone shifted further after global yields climbed late in the week amid renewed rate hike concerns in the United States.

Rising global yields and heightened risks tied to the flood control corruption mess and uncertainty on government execution added a risk premium to longer-dated bonds, contributing to a modest bear-steepening of the curve, he added.

Market attention turned to the US after President Donald J. Trump signed legislation ending the 43-day federal government shutdown, restoring the release of key economic data.

“The resumption of US government operations refocused markets on the global rate narrative, particularly the Fed’s more hawkish-leaning rhetoric amid concerns over still-sticky inflation,” Mr. Ulpo said.

This week, he expects a defensive stance as investors weigh a mix of domestic governance risks, tepid growth and the prospect of tighter financial conditions abroad.

Mr. Agonia sees upward pressure on yields if the political fallout from the flood control scandal escalates. “Market participants should also look out for more signals from Fed officials regarding the possibility of a December cut,” he added.